You closed your activity a while ago — maybe to take a job, maybe for a break — and now you want to invoice as an independent worker again. Good news: reopening is as simple as opening for the first time.

But there is one question that always comes up and rarely gets a clear answer: “the Portal calls it Reinício de Atividade — is that going to cause me problems?” The short answer: no. Here is why, and what actually changes compared with the first time.

Início vs Reinício: are they the same thing?

When you reopen, the process is treated as a declaration of início de atividade — the same declarative act as the first time. On the Finance Portal, the path is the same: “Início de Atividade” → “Entregar declaração”, even if you have had activity before.

The confirmation document you receive may carry the title Reinício de Atividade, but it is the same kind of document, with the date of the new start. It is not a special or more complicated process. If a bank or third party asked you for an “início de atividade” declaration, this document does the job.

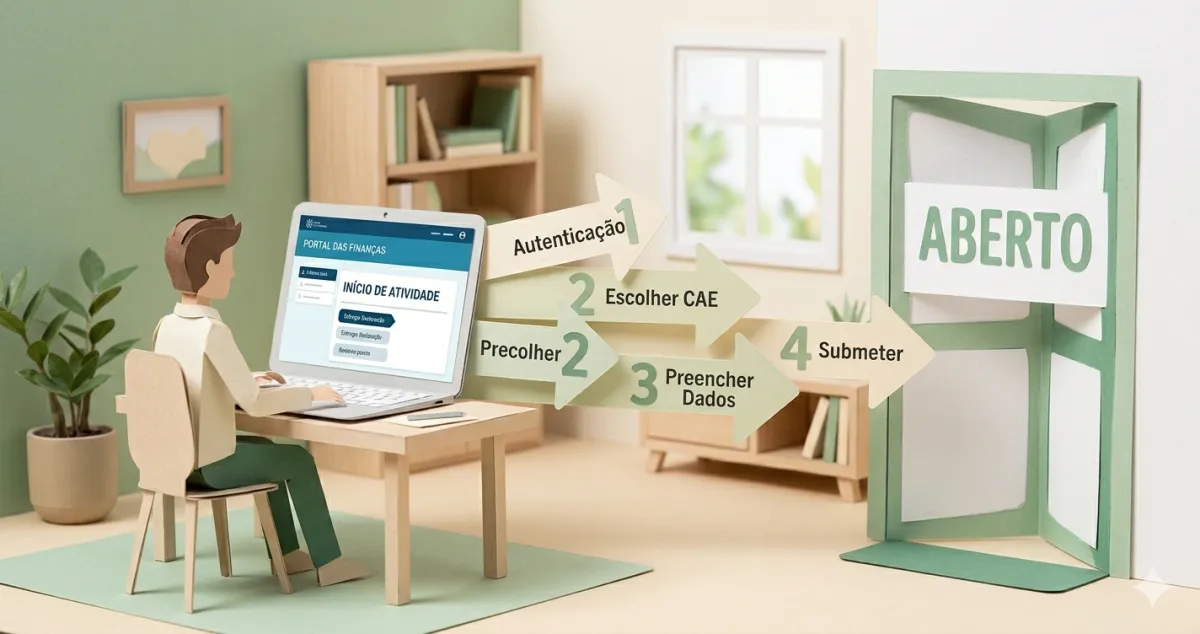

How to reopen — step by step

On the Finance Portal, it takes about 5 minutes:

- Log in with your NIF and password

- Serviços → Atividade → Início de Atividade

- Enter the start date (it must be today or a future date — it cannot be backdated)

- Select your CAE and taxation regime

- Submit and save the confirmation

If you are unsure about the general process, our complete guide to opening activity explains every step in detail — it applies equally to a reopening.

What changes compared with the first time

Here is the most important point, and the one most people do not know.

Social Security: the 12-month exemption does not restart from scratch

The first time you open activity, you get 12 months with no obligation to contribute to Social Security. That benefit is a one-off — it does not restart from scratch each time you reopen.

There is one important exception, though. If you closed within the first 12 months (before using up the exemption) and reopen within 12 months of the cessation, the count is paused and continues — you keep the exemption months you had not yet used. For example: you used 4 months, closed, reopen 3 months later → you still have the remaining 8 months.

Outside that case — if you had already used up the 12 months, or you reopen more than 12 months after closing — the obligation to contribute starts right away on reinício. There is no fresh 12-month period.

VAT: you can return to the Article 53 exemption (with exceptions)

As a rule, when you reopen you can opt back into the Article 53 VAT exemption if your estimated invoicing stays below €15,000. That estimate is for the current calendar year — from the start date to year-end, not annualised. Eligibility also depends on your previous calendar year’s turnover, where applicable.

But watch out for a rule that catches many people (Article 56 of the CIVA). There are two cases where you cannot return to the exemption straight away, even with forecast invoicing below €15,000:

- If you were in a taxation regime (normal regime) at the date of cessation and you reopen within the following 12 months;

- If you reopen in the year after cessation and, had you not closed, you would have moved to the normal regime because of the previous year’s turnover.

If you fall into either case, you either wait out the required time, or open on the normal regime and switch to the exemption later, at the proper moment.

The CAE and the regime

Reopening is a fresh declaration, so you select the CAE and regime again. If your activity is the same as before, you choose the same code. If it has changed, this is your chance to get it right — see the CAE and CIRS guide if you are unsure.

Two myths to avoid

Two ideas circulate that can land you in trouble:

❌ “I’ll close and reopen to change my VAT regime”

It does not work, and it backfires. Changing from the normal regime to the Article 53 exemption is done through a Declaração de Alterações in January (Article 32 and 54(2) of the CIVA), not by closing and reopening.

Worse: closing and reopening just to change regime triggers a rule that blocks you from the exemption for 12 months. Instead of fixing things, you create a problem. If you want to change regime, wait for January and use the alterações declaration.

Note: if you voluntarily opted into the normal regime (renunciation of the exemption), you are required to stay in it for at least 5 years — you can only leave earlier in the case of an essential change to your activity conditions (Article 55 of the CIVA).

❌ “I’ll reopen with a backdated date to invoice old work”

This is not possible either. The start date of a reopening must be the day you submit or a future date — never a past date. And you cannot issue an ato isolado in the year you closed your activity or the year after — in those cases, reopening activity is the only route. If you need to invoice recent work, talk to an accountant about the correct route before proceeding.

Frequently asked questions

Is Reinício de Atividade different from Início de Atividade? In practice, no. It is the same declarative act and the same document, with the date of the new start. The title may say “Reinício”, but it serves the same purposes.

How many times can I reopen? There is no limit. You can close and reopen as your situation requires — it is completely normal.

Do I keep my NIF? Yes. The NIF is your taxpayer number and never disappears, whether your activity is open or closed.

Do I get the 12 months without Social Security again? You do not start a fresh 12-month period. The exception: if you closed before using up the initial exemption and reopen within 12 months, you keep the months you had not yet used.

✅ In summary

-

Reopening is the same process as opening — Finance Portal, “Início de Atividade”, 5 minutes. The confirmation may be called “Reinício”, but it is the same document.

-

The 12-month Social Security exemption does not restart from scratch — but if you closed within that period and reopen within 12 months, you keep the months left over. Otherwise, you contribute from the reinício.

-

Do not use close+reopen to change regime or for backdated dates — it does not work and can block your exemption. To change your VAT regime, use the alterações declaration in January.

-

With FIZ everything is automatic again from day one — invoices, quarterly declarations, and reminders of your obligations, without you having to think about them.