It’s September. You open the app or the spreadsheet, add up what you’ve invoiced since January — and the number is €15,400.

Your heart sinks. You were VAT-exempt. Now what?

Take a breath. You need to act, but this is a problem with a clear solution.

What it means to exceed €15,000

When you opened your activity, you probably chose VAT exemption under Article 53 of the Portuguese VAT Code — which lets you invoice without charging VAT as long as your annual turnover stays below €15,000.

When you cross that threshold, Portuguese law distinguishes two scenarios under Article 58 of the VAT Code:

Scenario A — You exceed €15,000 but stay below €18,750: The move to the standard VAT regime only takes effect on 1 January of the following year. You continue invoicing without VAT until then. You have 15 business days from the last day of the year to notify the tax authority.

Scenario B — You exceed €18,750 (more than 25% above the threshold): The effect is immediate. The very invoice that pushes you past €18,750 must already include VAT. You have 15 business days from that moment to notify the tax authority.

Example: Sofia invoiced €14,800 by September and issues a €500 invoice. Her total becomes €15,300 — above €15,000 but below €18,750. This is Scenario A: she continues invoicing without VAT until 31 December and moves to the standard regime in January.

If that invoice had been €4,000 and pushed the total past €18,750 — she’d be in Scenario B and would need to charge VAT from that invoice onwards.

What to do — step by step

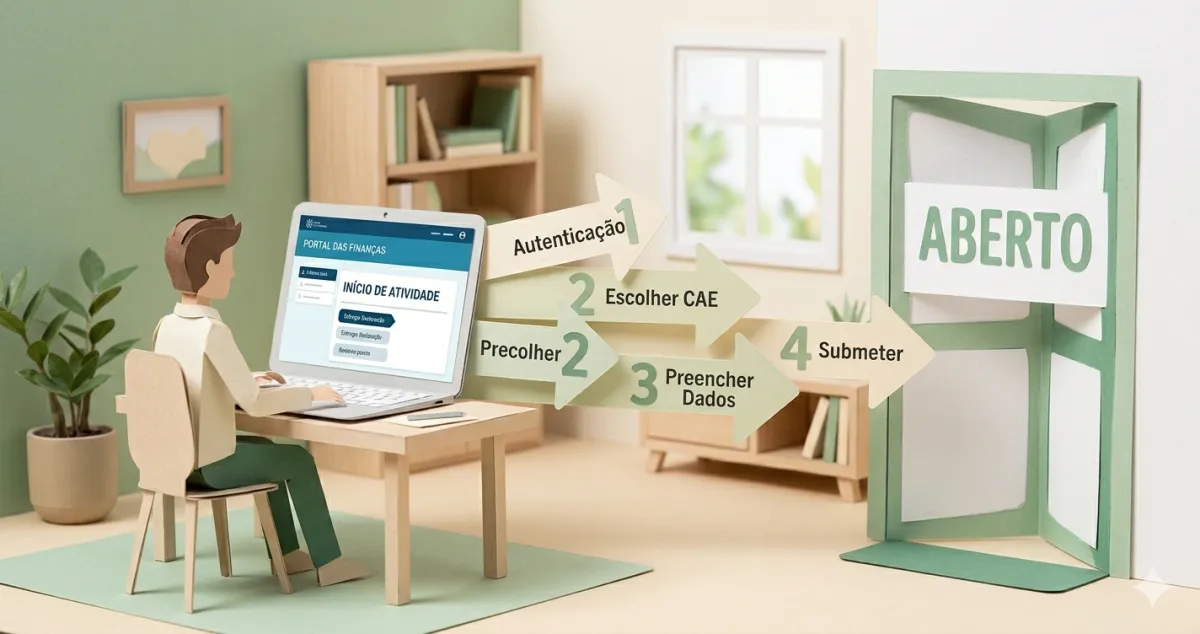

1. Notify the tax authority (within 15 business days)

You have 15 business days to submit an amendment declaration on the Portal das Finanças:

- Go to “Serviços” → “Atividade” → “Declaração de Alterações”

- Indicate that you’re moving from the exemption regime to the standard VAT regime

- Submit

2. Start charging VAT on the next invoices

For most services, the standard rate is 23%. The client now pays your amount + VAT.

Before: €1,000 for the project After: €1,000 + €230 (23% VAT) = €1,230

Important: the €230 in VAT is not yours. It belongs to the state, and you must remit it quarterly.

3. What about previous invoices?

You don’t need to redo anything. Invoices issued before you crossed the threshold remain correct — they were issued under a valid exemption.

The new quarterly obligations

Once you move to the standard VAT regime, you must submit the periodic VAT declaration every quarter.

The deadline: by the 20th of the 2nd month following the end of each quarter:

- Q1 (Jan–Mar): by 20 May

- Q2 (Apr–Jun): by 20 September

- Q3 (Jul–Sep): by 20 November

- Q4 (Oct–Dec): by 20 February

The amount to remit is: VAT charged to clients — VAT paid on your professional expenses.

Example: Ana charged clients €690 in VAT during the quarter. On her expenses (equipment, software) she paid €120 in VAT. She remits to the state: €690 − €120 = €570.

The impact on your business

Moving to VAT has practical implications worth planning for:

Prices increase for private clients — a private client who used to pay you €500 now pays €615. Some clients may question the increase. Prepare your explanation.

For business clients, the impact is smaller — companies deduct the VAT they pay you, so the actual cost to them stays the same.

Cash flow — the VAT you collect isn’t fully yours. When you receive €1,230, set aside €230 for the state immediately. Even if the client delays payment, the tax authority’s deadline doesn’t move.

How to avoid nasty surprises in future

The problem isn’t crossing €15,000 — it’s not knowing it’s happening until it’s too late.

Track your cumulative invoicing every month. When you reach €12,000, start planning the transition: alert clients, update quotes, prepare the notification process.

With FIZ, the dashboard always shows your accumulated invoicing and alerts you as you approach the threshold. When you cross it, quarterly VAT declarations are submitted automatically — no extra deadlines to manage.

⚠️ If it’s been weeks since you crossed the threshold: act today. Submit the amendment declaration, start charging VAT, and regularise any missing declarations. The longer you wait, the larger the potential fine.

✅ In summary

-

Two scenarios apply: if you stay between €15,000 and €18,750, you continue without VAT until 31 December and notify the tax authority within 15 business days after year-end. If you exceed €18,750, the obligation is immediate — notify within 15 business days and charge VAT from that invoice onwards.

-

The standard rate is 23% on the value of services. VAT collected is remitted quarterly, minus VAT paid on your own expenses. Deadlines are the 20th of the 2nd month following each quarter (20 May, 20 September, 20 November, 20 February).

-

With FIZ you can track your cumulative invoicing in real time — and when you move to the standard VAT regime, quarterly declarations become automatic. No risk of missing a deadline.