Sofia is a graphic designer. She creates logos, visual identities, and marketing materials. But a few months ago she started running Illustrator workshops — and suddenly she was earning €500/month from training.

“Do I need another CAE code now? Will I have problems with the tax authority?”

No. But there are a few important details.

You can hold multiple CAE codes simultaneously

The CAE code (Classificação das Actividades Económicas — Economic Activity Classification) is how you tell the tax authority what you do. Design is one thing, training is another, consultancy is another still.

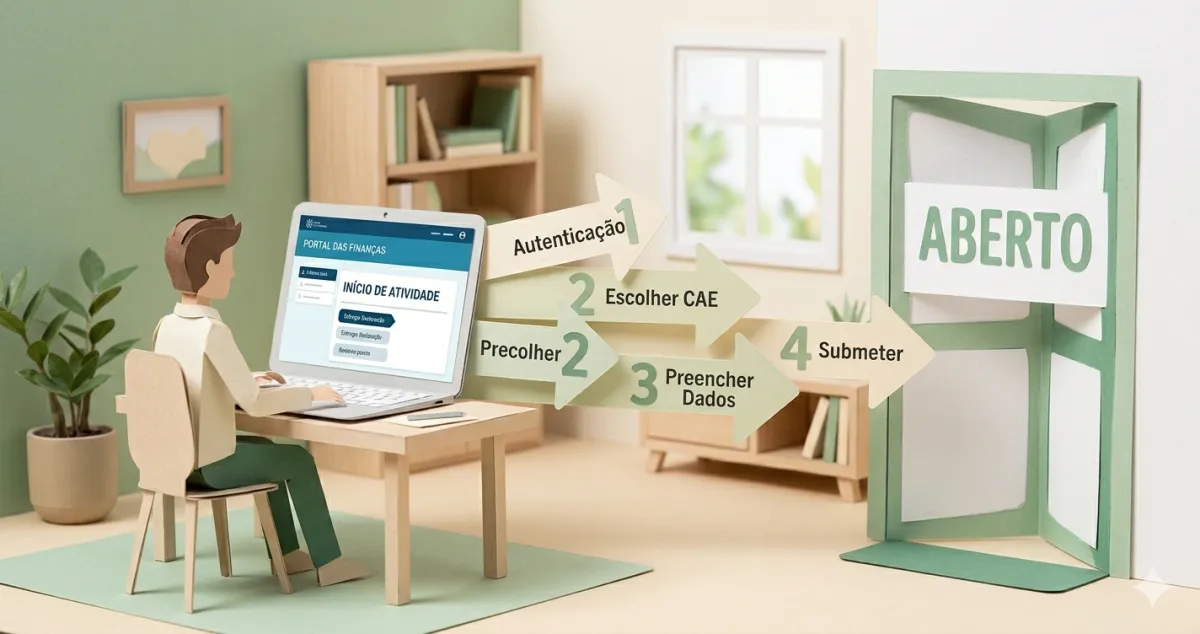

You can have one primary code and add secondary codes at any time, directly on the Portal das Finanças:

- “Serviços” → “Atividade” → “Declaração de Alterações”

- Add the new CAE code as a secondary code

- Submit

From that point, you can invoice under the new code. Legal, normal, and very common among freelancers who diversify.

Not sure which code to choose for each activity? See the table of CAE and Article 151 codes by profession — designers, lawyers, trainers, musicians and more, with a live finder for the full Article 151 table.

The detail that changes everything: income tax coefficients

Here’s the part most people don’t know.

Under the simplified regime, different activities have different coefficients — meaning different percentages of income are considered taxable for income tax purposes:

| Activity type | Coefficient | % taxable |

|---|---|---|

| General services | 0.75 | 75% |

| Product sales | 0.15 | 15% |

| Hotel/accommodation activities | 0.35 | 35% |

Practical example: João does consultancy (coefficient 0.75) and also sells templates online (coefficient 0.15). If he invoiced €10,000 in consultancy and €2,000 in sales:

- Taxable from consultancy: €10,000 × 0.75 = €7,500

- Taxable from sales: €2,000 × 0.15 = €300

- Total taxable: €7,800 (instead of €9,000 if everything were services)

The difference is real — and it only works if each invoice carries the correct CAE code.

How it works in practice

When you issue an invoice in certified billing software, you select the CAE code corresponding to the service provided.

- Consultancy to a restaurant → consultancy CAE

- Design workshop → training CAE

- Template sale → sales CAE

The system automatically applies the correct coefficient to each invoice. At year-end, the tax authority adds everything up and taxes accordingly.

The most common mistake: always using the same CAE code regardless of what you’re invoicing. The tax authority may question it, and you’re potentially missing out on a legitimate tax advantage if you mix up different coefficients.

Quarterly declarations don’t get more complicated

Good news: having multiple CAE codes doesn’t multiply your obligations.

You still submit:

- One quarterly VAT declaration

- One quarterly Social Security declaration

- One annual income tax return (with everything consolidated in Annex B)

What changes is that your billing software — in your case FIZ — automatically separates income by CAE code and calculates the correct coefficient for each one.

✅ In summary

-

You can hold multiple CAE codes simultaneously — it’s legal, it’s normal, and adding them is straightforward on the Portal das Finanças. Each code represents a different activity.

-

Income tax coefficients vary by activity — general services (0.75), product sales (0.15), accommodation activities (0.35). Each invoice must carry the correct CAE code so the system applies the right coefficient.

-

With FIZ the process is transparent — you select the code on each invoice, the system applies the coefficient automatically, and you get separate statistics per activity so you can see what earns the most.