You received a quote request from a German company or a client in Brazil. Good news — but immediately after comes the question: VAT or not? What NIF do I use? What currency do I invoice in?

The rules depend on two factors: where the client is and whether they are a business or an individual.

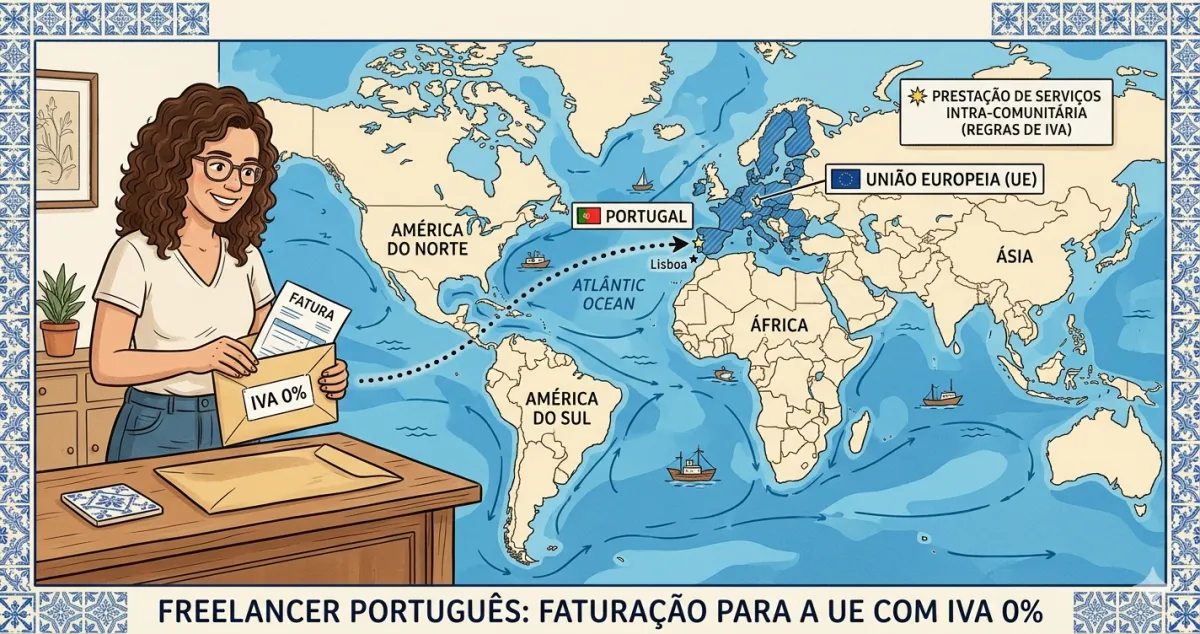

Case 1: company in the European Union (B2B)

Rule: you do not charge VAT. The client pays VAT in their country — this is called the reverse charge mechanism.

On the invoice:

- Client’s EU VAT number (starts with the country code: DE for Germany, FR for France, etc.)

- VAT: 0% — reverse charge / Art. 6 CIVA

- Mandatory note: “VAT — reverse charge by the acquirer”

What you need to do beyond invoicing: If you are not VAT-exempt in Portugal, you must report these service supplies in your periodic VAT return and in the Recapitulative Statement (annual intra-Community operations declaration).

Tip: always verify the client’s EU VAT number on the VIES system (ec.europa.eu/taxation_customs/vies) to confirm it is valid.

Case 2: private individual in the European Union (B2C)

Rule: you charge Portuguese VAT normally — 23% for general services.

Exception: if total B2C sales to the EU exceed €10,000/year, you may need to register for the OSS (One Stop Shop) scheme and pay VAT in the client’s country. For most Portuguese freelancers this does not apply.

Case 3: client outside the European Union (USA, UK, Brazil, Switzerland, etc.)

Rule: no VAT — these are service exports.

On the invoice:

- Use 999999990 (code for non-residents without a Portuguese NIF)

- VAT: 0% — export of services / Art. 6 CIVA

No special reporting obligations for non-EU clients beyond the standard filings.

VAT rules summary

| Client type | VAT on invoice | Reason |

|---|---|---|

| EU company (B2B) | 0% | Reverse charge |

| EU individual (B2C) | 23% | Portuguese VAT |

| Any non-EU client | 0% | Export of services |

Important note: if you are VAT-exempt in Portugal under Art. 53 CIVA (annual invoicing < €15,000), this table simplifies: you always apply 0% to all clients, domestic and foreign, with the Art. 53 exemption reason.

What currency to invoice in?

You can invoice in any currency — dollars, pounds, Swiss francs. What matters for Portuguese tax purposes is the value in euros.

Recommended practice: invoice in euros whenever possible. If the client insists on another currency, convert at the day’s exchange rate and record the euro value in your invoicing system.

IRS with foreign clients

Foreign clients do not withhold Portuguese income tax. That is always your responsibility. You receive the full amount and pay all the IRS in your annual declaration.

✅ In summary

-

EU company = 0% VAT with reverse charge; EU individual = 23% VAT; non-EU client = 0% VAT.

-

Foreign clients do not withhold Portuguese income tax — you receive everything and pay the tax in your annual declaration. Always set aside 15–25% of each invoice.

-

With FIZ the software identifies the client type and automatically applies the correct VAT rules — you do not need to memorise the distinctions for each situation.