Last night, Maria was at a café with friends. Between drinks, she mentioned she had just opened her freelance activity as a designer. The lively conversation died instantly. “What about VAT?” asked João. “You’ll have to charge 23% on everything!” said Ana. “Watch out for the fines!” warned Pedro. Maria went home with a knot in her stomach — and it was not the beer.

If you are a freelancer in Portugal, you have probably been there. VAT sounds like a monster that will eat your business. Spoiler: it is not. Once you understand how it works, you will find it simpler than paying for coffee with your phone.

The fact that changes everything: you may be VAT-exempt

Here is the key point: if you invoice less than €15,000 per year, you can be exempt from VAT under Article 53 of the CIVA. Zero VAT. You do not charge clients, do not pay the state, and do not file periodic VAT returns.

How does it work? When you open your activity, you choose the exemption regime. On every invoice you issue (always through certified software), you select 0% VAT and indicate the reason: “Article 53 CIVA.” The software generates the invoice with all legally required codes.

Tiago, a wedding photographer, discovered this in his first year. He invoiced €12,000 and never had to deal with VAT. “It was like a weight off my shoulders. I could focus on my work without worrying about quarterly VAT declarations.”

For those who invoice more: VAT is not your money

Imagine your business grows and you cross the €15,000 threshold. First: breathe. VAT is not a tax you pay from your own pocket. You are simply the middleman. Here is how it works:

- You do a job for €1,000

- You charge the client €1,000 + €230 VAT (23%) = €1,230

- The €1,000 is yours

- The €230 you hold and pass on to the state

Sofia, a marketing consultant, explains it to her clients this way: “My service price is €1,000. VAT is an extra the state charges — not me. Like a service charge at a restaurant: it doesn’t go to the waiter, it goes to the house.”

The three VAT rates (and when to use each)

Portugal has three main VAT rates:

- 23% — the standard rate. Applies to most services: design, consulting, programming, marketing

- 13% — the intermediate rate. Rarely used by freelancers (some food service and accommodation)

- 6% — the reduced rate. Specific services such as certified professional training

In day-to-day work, you will almost always use 23%. If you are unsure which rate applies to your service, check the official AT guidance — applying the wrong rate can cause problems.

The quarterly VAT return: simpler than it sounds

If you are not exempt, you file a quarterly VAT return — four per year, one every three months. Inês, a translator, used to dread these. Reality? “You fill in a few fields with your invoice totals. The Finance Portal does the maths.”

The process on the Finance Portal:

- “Entregar” → “Declarações” → “IVA”

- Enter your invoice totals

- The system calculates what you owe (or are owed as a refund)

- Submit

With the right software, this declaration can be submitted automatically.

The VAT you can reclaim on expenses

If you are VAT-registered, you can deduct the VAT you pay on professional expenses. Bought a laptop for €1,230 (€1,000 + €230 VAT)? That €230 can be offset against the VAT you owe the state.

Practical example:

- You charged clients €500 in VAT during a quarter

- You paid €200 in VAT on professional expenses (equipment, software, etc.)

- You only pay the state: €500 − €200 = €300

Note: This deduction only applies if you are VAT-registered. If you are exempt under Article 53 CIVA, you cannot reclaim input VAT on expenses.

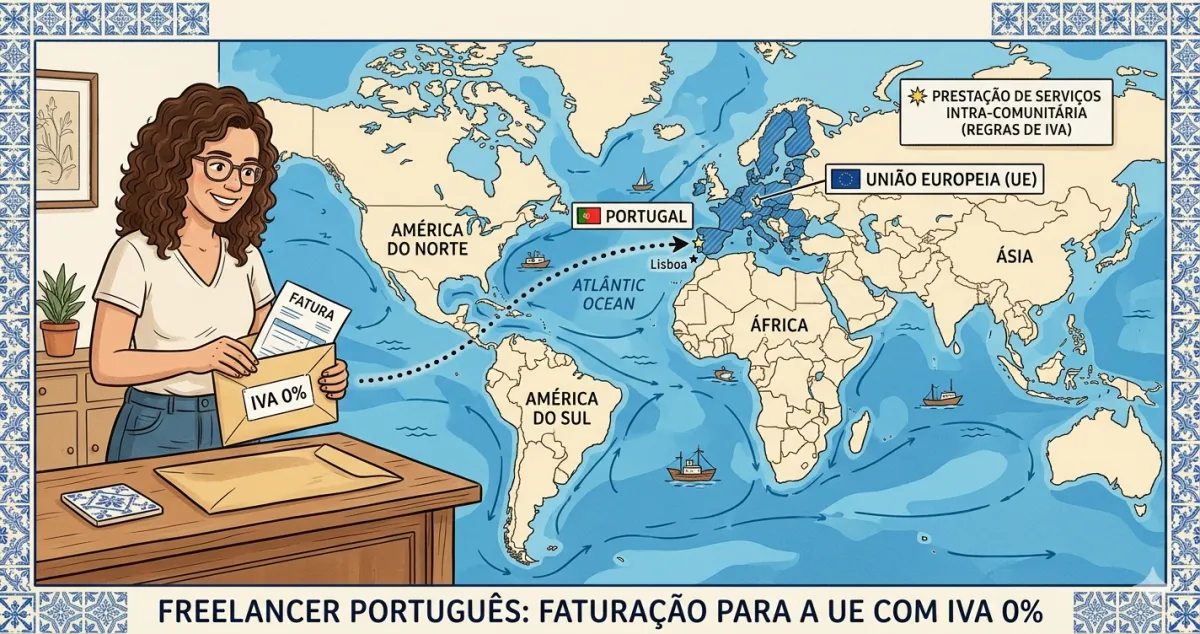

Working with foreign clients

Rita, a copywriter, works mostly with international clients. She expected complications. It turned out to be simpler than she thought.

For business clients within the EU (with a valid VAT number):

- You charge 0% VAT

- You select “reverse charge” as the reason

- You must file the quarterly Recapitulative declaration

For clients outside the EU:

- You charge 0% VAT

- You select the appropriate exemption

- No Recapitulative declaration required

✅ In summary

-

If you invoice less than €15,000 per year, you can be VAT-exempt under Article 53 CIVA — no complications, no periodic VAT returns to file.

-

VAT is not your money — you collect it from clients and pass it on to the state. You are the middleman, not the one paying.

-

With FIZ the quarterly VAT return is filed automatically — so you can focus on your work without keeping track of deadlines.