You’re wrapping up a project with a German company. Do you charge VAT? The answer depends on a single number: their EU VAT number.

The basic rule: reverse charge

When you provide B2B (business to business) services to a company in another EU country, VAT isn’t charged by you — it’s self-assessed by the client in their own country.

In plain terms: you don’t add VAT to the invoice. The European client declares and pays VAT in their own country, at their own rate.

But for this to work, you need the client’s VAT number.

What is a European VAT number?

It’s the company’s tax identification number for intra-community VAT purposes. The format is:

Country prefix + number — for example:

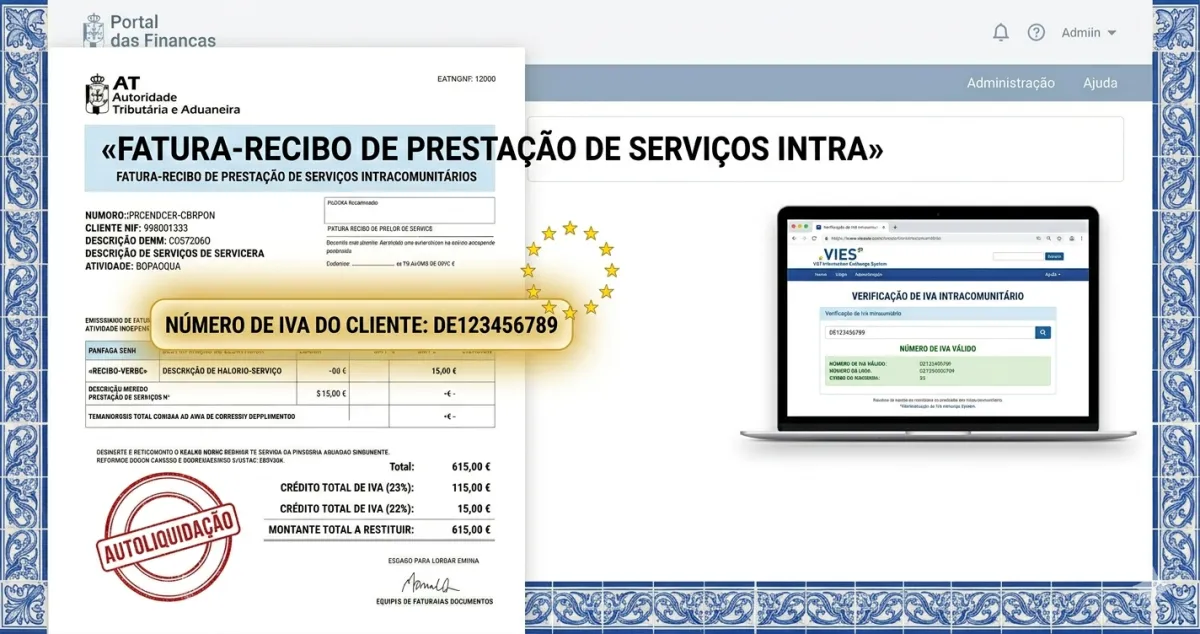

- Germany: DE123456789

- Spain: ES12345678A

- France: FR01234567890

- Italy: IT01234567890

- Netherlands: NL123456789B01

Each country has its own specific format, but the principle is always the same: country code + numeric (or alphanumeric) sequence.

How to verify the number is valid

Before issuing an invoice without VAT, verify the client’s VAT number on VIES — the European Commission’s official system:

🔗 vies.ec.europa.eu

Enter the country and number. VIES confirms whether the company is registered for intra-community VAT. If it isn’t — you must charge VAT.

What happens if you don’t ask for the number?

If you don’t have the client’s VAT number → you must charge Portuguese VAT (23%).

The European client can eventually recover that VAT — but it’s a bureaucratic process for them. And you have to declare it and remit it to the tax authority.

Without the VAT number, the reverse charge mechanism doesn’t apply.

How to ask the client

No complicated explanation needed. Simply say:

“To issue the invoice without VAT under the reverse charge mechanism, I need your EU VAT number. Could you send it to me?”

Most European companies are familiar with this process — it’s standard practice in intra-community trade.

How it appears on the invoice

When you issue an invoice with the client’s VAT number:

- VAT: 0% (or exempt)

- Note on invoice: “Reverse charge applies — Article 6 CIVA”

- The client’s VAT number should appear in the invoice header

Recapitulative declaration

When you issue invoices without VAT to European companies, you must report those clients quarterly in the Declaração Recapitulativa (Recapitulative Declaration on Portal das Finanças).

This declaration lists all EU clients and the amounts invoiced — it’s mandatory and follows the same deadline as the VAT declaration (20th of the 2nd month after the quarter).

✅ In summary

-

Whenever you invoice an EU company, ask for their VAT number before issuing. Verify on VIES (vies.ec.europa.eu). With a valid number, you issue without VAT (reverse charge).

-

Without the VAT number, you charge Portuguese VAT — 23% you must remit to the tax authority. More work for you and for the client.

-

With FIZ the recibo verde already includes intra-community logic — enter the client’s VAT number, it applies the correct exemption and automatically includes the amount in the quarterly recapitulative declaration.